- This article is provided for Educational Purposes only -

Highlight

This article presents why World Bank Group support for state-owned enterprise (SOE) reform matters, the pattern of Bank Group engagement, and a typology of major Bank Group support interventions. It assesses the contribution of the World Bank Group’s three main institutions to enhancing development outcomes through their support of SOE reform: what works and what does not, the effectiveness of the Bank Group’s various approaches, factors that explain success and failure, and the strengths and weaknesses of the Bank Group’s approach. To allow for greater depth, it focuses on two leading sectors for SOE support: finance and energy. SOEs play a major role in many developing and emerging economies, where governments use them to achieve economic, social, and political objectives: to deliver and extend access to services, fill gaps in markets, develop key sectors or regions, and provide employment. However, the mixed institutional mandates of SOEs and their political importance often pose performance and governance challenges. This can mute transparency and accountability, making oversight and regulation difficult. The Bank Group, from fiscal years 2008 through 2018, initiated 1,008 projects with 2,187 components (interventions) that supported the reform of SOEs in the financial and energy sectors, with an estimated combined value of $71.7 billion in financing. This involved financial, technical, and advisory support for both policy and institutional reforms (upstream) and enterprise-level activities (downstream). This evaluation focuses on five major types of reforms: corporate governance; business and operations; strengthening competition and regulation in SOE markets; privatization and other ownership reform; and macro, fiscal, and public financial management reforms.Evaluation Purpose and Scope

State-owned enterprises (SOEs) have distinctive characteristics, including control by the state, legal and financial autonomy from the state, and participation in the productive sector (Raballand et al. 2015). Corporate control may be exercised through ownership, administrative and technical management, interlocking of directorates, and regulatory oversight (Farazi, Feyen, and Rocha 2011). Unlike public agencies, SOEs benefit from a level of autonomy because of their productive activity. Special laws that are different from private sector laws often govern SOEs (World Bank 2014a).

Study Case 1 - State-Owned Enterprises in the Response to the Coronavirus Pandemic

SOEs play a critical role in the energy and financial sectors in many developing and emerging economies. Most countries still depend on SOEs to provide power. SOEs accounted for 71 percent of the Morgan Stanley Capital International (MSCI) Emerging Market Index in utilities, 56 percent in energy, and 39 percent in the financial sector in 2020. State control is prevalent in the oil and gas sector, with about 90 percent ownership of reserves and 55 percent of production. Although state ownership in commercial banks declined from 67 percent of total banking assets in 1970 to 22 percent in 2009, SOEs often retain a dominant role in banking (World Bank 2012a). In emerging markets such as China and India, SOEs hold more than half of banking system assets (Bank Group 2012). Singapore successfully used SOEs to drive development and industrialization after its independence in 1965, with successes in diverse fields including oil refining, petrochemicals, and development finance (PwC 2015). Governments use SOEs to pursue economic, social, and political objectives alongside their commercial objectives.1 The mixed objectives demanded of SOEs can include contribution to employment creation, poverty alleviation, fiscal stability, spatial or sectoral development, environmental protection, and sector regulation. For example, India relied primarily on state-owned financial institutions (SOFIs) to implement its Jan Dhan Yojana program, under which about 300 million basic accounts were opened in a short period. In Kenya, the Kenya Power and Lighting Company was the main vehicle for the government’s drive for universal electricity access, achieving more than 1 million new connections a year. During the coronavirus pandemic, many governments have used SOEs to channel resources to adversely affected firms and households (box 1.1). Some SOEs have been run well and have made important contributions to economies.SOEs’ multiple objectives pose several governance and management challenges. Mixed objectives and weak oversight obscure accountability, exacerbate principal-agent challenges, and weaken incentives for performance (box 1.2). SOEs also reflect the desire of the state or political groups to exert political influence over economic outcomes and resource allocation. Although some SOEs are run well, many others suffer from low productivity and efficiency and have a detrimental impact on growth and consumer access to services. Poor financial performance and management practices can generate substantial public fiscal losses, debt, or contingent liabilities.2 SOEs frequently lack adequate governance oversight arrangements, regulation, and levels of transparency and disclosure, which can foster mismanagement, corruption, and underperformance.3 Yet SOEs can also impose barriers to private participation in sectors where their dominant presence enables anticompetitive behavior, often with government protection or subsidy.4

Study Case 2 - Three Perspectives on State-Owned Enterprises in the Literature (Not Mutually Exclusive)

Evaluation Approach

This evaluation assesses the contribution of the Bank Group’s three main institutions from fiscal year (FY)08 through FY18 to enhancing development outcomes through their support of SOE reform. In this evaluation, the focus is limited to support intended to improve SOE performance at the national, sectoral, or enterprise level, where it imposes a constraint on development. The evaluation excludes interventions where SOE reform was not the challenge being addressed, but rather SOEs were used as an instrument to address a development challenge (such as when a line of credit is channeled through a state-owned bank; World Bank 2019f). To allow for greater depth, the evaluation focuses on the two leading sectors for SOE reform support (identified at the approach stage): the financial sector and the energy sector. The evaluation answers four questions:

- What is the Bank Group doing to support SOE reform?

- How effective are Bank Group SOE reform interventions, and where are these strengths or gaps?

- What internal (directly under the Bank Group’s control) and external factors explain the success or failure of Bank Group SOE reform interventions?

- Does the Bank Group have a robust approach to achieving development impact through SOE reform, considering client priorities and needs and its own goals and principles?

To answer these questions, the evaluation employs a theory of change (Appendix A) to inform the analysis using mixed methods with quantitative and qualitative evidence:

- The analysis is multilevel, looking at country, sector, project, engagement area, and intervention mechanisms, covering both upstream SOE reforms (policy, regulatory, and institutional) and downstream SOE reforms (enterprise level). It excludes Bank Group projects that use SOEs to deliver services without trying to reform them.

- The mixed methods include portfolio review and analysis, eight country case studies, subject and sector deep-dive studies, a structured literature review, a review of country strategies and diagnostics (including Financial Sector Assessment Programs), and an econometric analysis.

The financial and energy sectors each have unique features and challenges:

- In the financial sector, there are state-owned commercial banks (typically taking deposits and offering credit and other services), development banks (financing public development priorities), and nonbank financial institutions in areas like insurance and pensions. Government ownership of financial institutions is understood to have the potential both to overcome market failures in promoting socially and economically desirable investments and to provide a vehicle to channel finance to strategically important sectors or firms. The Bank Group understands national development banks to be key “to help crowd-in the private sector to finance projects with high developmental impacts such as infrastructure or projects that can yield a greater public good but which the private sector may not be interested in funding directly” (Pazarbasioglu2017). Challenges include the performance of such institutions in practice, the difficulties of aligning their actions with policy intentions, and the effects of such institutions on financial system competition, efficiency, and stability.

- Within the energy sector, the evaluation covers power companies (often utilities) involved in distribution, generation, or transmission and those engaged in energy extraction. A recent World Bank reconsideration of its approach to power sector reforms recognizes that “among the best-performing power sectors in the developing world are some that fully implemented market-oriented reforms, as well as others that retained a dominant and competent state-owned utility guided by strong policy mandates, combined with a more gradualist and targeted role for the private sector. This reality makes a case for greater pluralism of approaches going forward” (Foster et al. 2020). Recent World Bank work suggests that in less institutionally mature environments, private sector participation is best limited to power generation.5 However, the literature (appendix G) finds governance and operational challenges for many power sector SOEs: financially unsustainable tariffs; mandated cross-subsidies; weak or inefficient regulatory environments; poor sectoral planning; high network losses, hidden costs or liabilities; or ambitious government access goals lacking adequate subsidization. Traditionally, the power sector was regarded as a natural monopoly, but technological advances and the identification of huge deadweight losses have changed this; yet few governments or regulators explicitly monitor the adequacy and reliability of energy supply, let alone require their disclosure. Professionalization of SOE staff is also challenging.

Five Types of Bank Group Support for SOE Reform

From FY08–18, the Bank Group initiated 1,009 projects with 2,187 components (interventions) that supported the reform of SOEs in the financial and energy sectors, with an estimated combined value of $71.7 billion in financing.6 This involved financial, technical, and advisory support for both policy and institutional reforms (upstream) and enterprise-level activities (downstream). To analyze these projects, the Independent Evaluation Group (IEG) took a representative sample of 88 percent of World Bank, International Finance Corporation (IFC), and Multilateral Investment Guarantee Agency (MIGA) financing and IFC advisory projects (374) and 20 percent of World Bank advisory services and analytics (ASA) projects (116 sampled). This maps to a total portfolio of 421 financing projects plus 1,184 World Bank ASA projects. Within the financing projects, 893 interventions (components) were within the scope of this evaluation. To expand the pool of evaluated SOE reform projects, IEG also analyzed 132 qualifying projects evaluated between FY08 and FY19 but approved between FY02 and FY07.

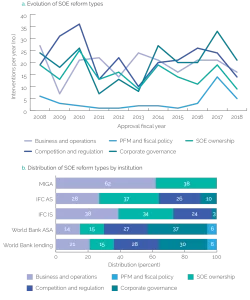

This evaluation focuses on five major types of SOE reforms supported by Bank Group operations and activities (figure 1.1).These reforms are corporate governance; business and operations; competition and regulation; privatization and other ownership; and macrofiscal, and public financial management (PFM). Together, interventions in these areas compose 87 percent of both interventions and financing for SOE reform and are components of 96 percent of projects identified as being in scope. The interventions can be complementary if more than one is used to achieve deeper reform. As shown in Figure 1, there is considerable year-to-year variation in their use.

Figure 1 - Bank Group SOE Reform Support by Type, FY08-18, and by Institution (no ASA)

Source: Independent Evaluation Group portfolio review and analysis.

Note: The figures show that 217 interventions supported SOE corporate governance reform; 210 supported business and operation reform; 236 sought to improve competition and regulation (of which 126 supported regulation); 167 supported SOE ownership reforms (of which 49 supported privatization); and 40 supported macro-fiscal, policy, public financial management, and debt. Percentages may not add up to 100 due to rounding. ASA = advisory services and analytics; FY = fiscal year; IFC AS = International Finance Corporation advisory services; IFC IS = International Finance Corporation investment services; MIGA = Multilateral Investment Guarantee Agency; PFM = public financial management; SOE = state-owned enterprise.

Business and Operations Reforms

The largest share of Bank Group–supported reforms aims at improving SOEs’ operations and business practices. Reforms in business and operations aim to improve operational and financial performance and enhance service quality. Projects supporting business and operations reform compose 24 percent of SOE reform interventions but account for 50 percent of commitment value. They are the leading form of energy sector reform support and the second most popular form in the financial sector. By institution, these reforms are in almost 60 percent of MIGA guarantees, 40 percent of IFC SOE investments, and 20 percent of World Bank lending projects. Ten percent of Bank Group financing support to reform SOEs focused on strengthening their financial management, primarily targeting financial sustainability (including the restructuring or rehabilitation of debts), enhancing revenue collection, and strengthening creditworthiness or expanding financial options.7About one-third of Bank Group commitments in this category support physical infrastructure improvements (almost entirely for power companies), one-quarter support human resource management, 16 percent support service or product quality improvement, 14 percent support operational or process efficiency improvement, and 11 percent support organizational restructuring. In the World Bank, the Energy and Extractives Global Practice (GP) leads many of these commitments, focusing on improving the business and operations of individual state-owned energy companies. For example, in 2017, to strengthen the financing of Bangladesh’s power supply, MIGA provided a guarantee to Standard Chartered Bank for its loan to the SOE North-West Power Generation Company Limited in Bangladesh to build, install, and operate a 220 megawatt, dual-fuel, combined cycle power plant. In the financial sector, examples include a 2009 World Bank–financed Private Housing Finance Markets Strengthening Project (P112258) in Mexico, which aimed to improve the technical capacity of Sociedad Hipotecaria Federal, a SOFI, to expand access to lower-income groups. The SOFI gained capacity through reengineering, the creation of a new department, simplification of procedures, and improved risk monitoring. IFC complemented the World Bank project with advisory and fee-based services.

Corporate Governance Reforms

Corporate governance reforms are pursued to improve SOE performance where government intends to retain ownership or as a path to privatization. Enterprises, whether public or private, are known to perform better with the right combination of incentives and the institutions to secure those incentives.8 Corporate governance arrangements shape internal incentives, balancing a desire for managers to have enough discretion to run the company without unduly interfering with a desire to keep them accountable to the interests and objectives of owners and other stakeholders. Corporate governance reforms composed 24 percent of non-ASA Bank Group interventions in the portfolio and 12 percent of commitments, including 29 percent of World Bank lending, 11 percent of IFC advisory services, and 4 percent of IFC investment services. In addition, corporate governance reform is a subject of 38 percent of World Bank ASA interventions. For financial sector SOE reform, corporate governance reform is the most popular form of intervention, ahead of business and operations reform. In the power sector, the World Bank’s flagship study finds that many reform efforts began with the corporatization of power utilities (World Bank 2019c).

The Bank Group has long been a champion for good corporate governance of SOEs, both as a step toward divestiture and as a self-standing means to strengthen performance. Improved corporate governance is used to achieve other ends—for example, to improve performance, service delivery, financial sustainability, governance, and access to private capital—but is often described as a project objective on its own. Corporate governance reforms often involve the following elements:

- Clarifying SOE objectives;

- Improving the legal and regulatory framework for SOE governance;

- Strengthening the state’s role as owner or shareholder;

- Professionalizing SOE boards and management;

- Promoting the financial sustainability of SOEs; and

- Enhancing the transparency and accountability of SOEs.

Corporate governance reform may accompany corporatization (the establishment of SOEs as corporate entities), but it may also be applied to existing public companies.

Bank Group's efforts to strengthen the governance of SOEs date at least to the 1980s and were described influentially in a 1995 report (Muir and Saba 1995). More recently, in 2014, the Finance and Markets and the Governance GP teams jointly produced a tool kit on SOE corporate governance rooted in Organisation for Economic Co-operation and Development guidelines. In the SOE reform evaluation portfolio, the level of activity in corporate governance was strong but has fluctuated since FY14 (see Figure 1). IFC requires corporate governance analysis for every investment transaction as part of its due diligence process and strives for client commitment to good corporate governance practices, including protection of shareholder rights, accountability to investors and stakeholders, quality of the control environment, and disclosure and transparency practices.

Support for corporate governance is often bundled with other reforms because it is seen as a vehicle for enhanced access, efficiency, and quality of services. In the evaluation portfolio, sector reforms tend to focus on the enterprise level, and national-level support often sets standards or builds institutional capacity to regulate or implement policy. The World Bank’s work is most often led by Macroeconomics, Trade, and Investment; Finance, Competitiveness, and Innovation; and Energy and Extractives GPs. A high percentage but a small number of Governance GP interventions were in corporate governance. In Kenya, for example, improving the utilities’ corporate governance was a core element of Bank Group engagements in energy sector reform. Capacity-building assistance to improve corporate governance was provided to several SOEs in the electricity sector, including the generation company, the distribution company, and the transmission company. For example, the generation company, KenGen, benefited from a World Bank–supported, comprehensive Corporate Governance Assessment, which informed the KenGen Guarantee Project (P162422), which supports long-term private capital mobilization by the company through a commercial risk guarantee. In another financial sector example, IFC invested in the state-owned Sri Lanka Life Insurance Corporation, taking a seat on the board and working to strengthen corporate governance to improve the SOE’s credibility with investors in preparation for privatization.

Privatization and Ownership Reforms

Privatization, often recommended in analytic work, has shown a declining trend in financing. Privatization and ownership reforms are pursued to improve SOE performance where a government intends to relinquish all or some portion of its ownership. Beyond privatization, other ownership reforms include promoting public-private partnerships (PPPs) or other partnership arrangements, opening to private sector investment (including foreign investment in SOEs), and setting up new SOEs while liquidating old ones. Privatization and ownership reforms are employed to obtain many of the objectives of SOE reform, including improvement of competition, enterprise productivity, and innovation (for 24 percent of the Bank Group SOE projects); operational or financial performance (for 22 percent of projects); sectoral efficiency (22 percent); public finances (13 percent); and service quality or delivery (13 percent). Ownership reform is far more popular in energy (especially in generation) than it is in the financial sector. Privatization is often recommended in analytic work such as Financial Sector Assessment Programs (box 1.3); it has seen ups and downs over several decades (box 1.4) and has shown a declining trend in financing (figure 1.2), with no interventions for 2013 and 2018 and a parallel trend in commitments. This seems at odds with the intention of the Bank Group’s FY18 corporate strategic statement on Maximizing Finance for Development (MFD) and its embedded Cascade approach, which state a preference for reliance on private finance and private sector solutions. The MFD intends to harness “the power of the private sector and enhance market creation to meet the twin goals and the SDGs [Sustainable Development Goals].” The aim is to “help client countries pursue sustainable private sector solutions [where] they can help achieve development goals, while preserving scarce public resources where they are needed most” (World Bank 2017a).

Overall, for the entire evaluation period, ownership reforms constituted more than one-third of IFC’s investment interventions and more than 40 percent of its advisory interventions. One-third of MIGA guarantees also supported ownership reform, especially focused on power generation. SOE privatization support, which has waxed and waned over several decades (box 1.4), has been rare recently. For the World Bank, 14 percent of lending interventions and 15 percent of ASA for SOE reform supported ownership reforms of all types. In 2007, for example, IFC supported the privatization of the Energy Development Corporation (25839) in the Philippines, the largest producer of geothermal power. IFC also supported its capital expenditure program and improved corporate governance practices. In 2012, MIGA issued a guarantee (M1367) to support, in Indonesia, a PT Rajamandala Electric Power (an independent power provider) hydropower plant and transmission line investments against the risks of expropriation, transfer restriction, war and civil disturbance, and breach of contract covering the contractual obligations of PT Perusahaan Listrik Negara (the state electricity company) under the power purchase agreement.

Figure 2 - Interventions Supporting State-Owned Enterprise Privatization

Source: Independent Evaluation Group portfolio review and analysis, projected to population of projects.

Note: ASA = advisory services and analytics.

Study Case 4 - Pendulum Swings on Privatization in Bank Group State-Owned Enterprise Reform

Competition and Regulation in SOE Markets

Strengthening competition and regulation in SOE markets can help align the activities of SOEs with development and policy objectives and level the playing field between SOEs and potential private competitors. This area of reform is supported in more than one-quarter of World Bank lending and ASA and IFC investment and advisory services interventions. It is not a feature of MIGA’s work.

Regulation can shape sectoral pricing (29 percent of regulatory interventions) or support the enactment of new laws, regulations, or regulatory institutions (26 percent). Strong sector regulation can set the framework for private participation and shape incentives for efficient service delivery. Power sector reform often emphasizes creating and empowering an independent regulatory agency, with a strong orientation toward technically-driven tariff-setting procedures (Pardina and Schiro 2018). In the energy sector, reforms were more likely to focus on pricing (41 percent) and sector strategies (20 percent). Financial viability of the energy sector through cost recovery pricing is needed to attract private investment, ensure reliable supply, meet universal access targets, and minimize negative macro-fiscal impacts (Huenteler et al. 2017). Cross-subsidies built into tariffs add complexity to the policies and politics of pricing reforms. For example, the 2009 development policy operation (DPO) for Burkina Faso (P099011) supported an enhanced regulatory framework with a transparent tariff-setting mechanism for power SOEs, along with establishing a regulator. In the financial sector, reforms focused more on sector laws and regulations and institutions to enforce them for SOEs and other financial institutions. This was the case, for example, for the 2017 World Bank Myanmar Financial Sector Development Project (P154389).

Some regulatory reform interventions reset sector policy. A DPO for Senegal in FY13 (First Governance and Growth Support Project, P128284) sought to improve energy sector efficiency and service through the adoption of a new Energy Sector Development Policy Letter, an action plan, and a financial and operational utility restructuring plan. The letter addressed gaps in the energy sector's legal and regulatory framework for both the electricity and hydrocarbon sectors. In Vietnam, a series of Poverty Reduction Support Credits (PRSCs) and DPOs supported sector strategy reform. The PRSCs broadly supported the enactment of an electricity law while working to improve sector strategies for the gas and electricity subsectors and supporting the adoption of market-based pricing mechanisms for electricity. DPOs focused on key sector policy areas: development of a competitive power market, power sector restructuring, electricity tariff reform, and demand-side energy efficiency.

Competition work often seeks to remedy weak incentives for SOEs to behave efficiently and contribute to economic development through improved productivity. In many countries, SOEs enjoy substantial market power, which may extend to both markets for goods and services and input markets. This market power can arise from small market size (or poorly developed markets, weak regulations, and poor oversight of competition) or weak policies (or enforcement) governing the ownership and treatment of SOEs. Enhancing competition is known to improve the performance of enterprises, whether private or public.

The leading ways the Bank Group promotes competition are opening entry or actively crowding in the private sector, promoting PPPs and privatization, and reforming tariffs. Competition objectives are often interwoven with others. Although not all SOE activities are in competitive market segments,9 IEG’s portfolio review found 132 interventions seeking to strengthen competition, innovation, and productivity. Their frequency increased in the mid-2010s. IEG estimates that more than 125 World Bank ASAs had competition, innovation, or productivity objectives. The 2015 Sustaining Shared Growth development policy loan for Turkey (P146322) exemplifies such support to strengthen competition. It supported competition and transparency in the energy sector through the enactment of the electricity market law, which limits SOEs’ role in the sector and ensures the development of a competitive environment for electricity markets. The operation benefited from extensive analytical work. In 2005, IFC began assisting the Bank of Beijing through investment and advisory services to prepare it to compete regionally.

IFC has declared in recent years that it considers principles of competitive neutrality when reviewing SOE financing, but the treatment of competitive neutrality in IFC projects is uneven. Papers submitted to the Bank Group Board of Executive Directors in 2017 and 2019 embraced the competitive neutrality concept, clearly defined by the Organisation for Economic Co-operation and Development, which implies that the same rules of market behavior should apply to public and private firms, including the application of regulations and of competition law. This principle seeks to ensure a level playing field, where the SOE has no undue competitive advantage. IFC states that the attributes of competitive neutrality include that the SOE earns a commercial rate of return on goods competing with private businesses; the SOE’s pricing for commercial activities and public services should not “unduly” distort the playing field through subsidy; the SOE’s access to public contracts and other treatment in public procurement is “open, transparent, and nondiscriminatory”; and the SOE strives toward international standards and practices (IFC 2017).10 IEG reviewed project-related documents for seven recent IFC SOE reform projects and found that the treatment of competitive neutrality remains uneven, with some attention as early as 2012 and some omissions as recently as 2017. Only one project package treated all of IFC’s competitive neutrality criteria.11

MIGA’s approach to supporting cross-border investments into SOEs is anchored on three criteria: government control, public service, and the creditworthiness and financial viability of the SOE as a stand-alone entity. SOE investors are eligible for MIGA coverage provided they operate on a “commercial basis.” In considering whether an SOE investor operates on a commercial basis, at least with respect to the investment being covered, MIGA assesses several factors, including whether the SOE investor (i) operates on a self-sustaining basis, (ii) enjoys substantial autonomy from the government, and (iii) does not enjoy protection from competition or preferential treatment—factors that closely map to aspects of IFC’s competitive neutrality principle. SOE project enterprises receiving MIGA-insured investments need only be creditworthy and financially viable, as judged by MIGA’s credit risk assessment.12 In this respect, MIGA’s approach to SOEs is markedly different from IFC’s. IEG’s review of nine recent guarantees against the risk of nonhonoring of financial obligations involving an SOE found only one that addressed whether the SOE enjoyed protection from competition or preferential treatment.

In a limited number of countries, the Bank Group (through its Markets and Competition Policy cluster, involving both World Bank and IFC advisory staff) has incorporated competitive neutrality into its analytics, including its Markets and Competition Policy Assessment Tool (MCPAT). The MCPAT analysis examines three areas: antitrust rules and enforcement, procompetition market and sector regulation, and competition principles in broader public policies, including SOEs and competitive neutrality. In this context, MCPAT examines SOEs and their behavior, including whether the playing field is level and open; whether state aid or other unequal tax, regulatory, debt, or procurement treatment inhibits competition; and whether there is a clear separation of commercial and noncommercial activities. MCPAT aims to focus reform on areas that promote competition and crowd-in private sector activity. For example, the Senegal MCPAT finds that in groundnut processing and fertilizer production, SOEs are protected by “restrictive government regulations” in value chains that “are traditionally economic activities that can be carried out by the private sector more efficiently than by SOEs” (Pop and Corthay 2018). Since its introduction in 2016, MCPAT has been applied to only a few countries—Argentina, Kenya, Mauritania, Mexico, Peru, the Philippines, Senegal, Vietnam, and Ukraine—and the Western Balkans region. The link between this analytic work and World Bank operations is still developing. A competitive market framework is being incorporated into the Integrated SOE Framework that the Equitable Growth, Finance, and Institutions Practice Group’s SOE Working Group is developing as guidance for staff. A module based on MCPAT has been incorporated into several Country Private Sector Diagnostics (CPSDs).

Public Fiscal and Financial Management Reforms

For decades, the World Bank has addressed public financial issues where SOE finances (including liabilities) threaten fiscal soundness or stability. Thus, SOEs’ macro, fiscal, and public finance aspects become part of a broader policy dialogue between the World Bank and governments on managing public revenues, expenditures, debts, and liabilities. SOEs’ fiscal implications are created by the influence that their costs, revenues, and risks have on public revenues, expenditures, debt service obligations, or other liabilities. Thus, it is critical to understand SOEs’ potential direct and indirect impacts on state finances.

Interventions related to macrofiscal and PFM reform compose only 4 percent of the identified portfolio for the two sectors and appear only in World Bank activities. They make up 6 percent of both World Bank lending and ASA interventions. However, the identified portfolio underrepresents the overall World Bank level of SOE-relevant activity on fiscal soundness and PFM because they are often addressed at the national level, thus affecting all SOEs rather than being tied to a single sector. For example, SOFIs and utilities can both generate public liabilities that destabilize the macroeconomy, as in crises faced by Mozambique and Slovenia.13 Some SOEs (such as oil companies) also provide important revenues to the state. For example, a recent Bank Group analysis of Sri Lanka points to the state-owned business enterprise portfolio representing “significant fiscal costs and fiscal risks undermining the government’s fiscal consolidation efforts” (World Bank 2020a, 4). It recommends that the Ministry of Finance conduct a “systematic analysis of SOE financial statements, business plans, and investment proposals,” which “could help the government anticipate and mitigate fiscal risks to the budget” (72).

The Bank Group tackles SOE macrofiscal issues through analytical work, DPOs, and technical assistance. As Mozambique’s recent SOE debt crisis demonstrates, this may involve engagement at the national level to rationalize budgeting and public investment, constrain SOEs’ ability to incur debt, implement stronger systems of PFM, and more. In response to the hidden debt revelations in 2016, the World Bank launched a program to strengthen public investment and fiscal management, including debt and SOE fiscal risks. It modified ongoing development policy lending and joined a group of general budget support donors to promote concrete steps toward transparency and accountability for the hidden loans. An FY13 Myanmar development policy loan, for instance, aimed to reduce the budget deficit partly by legally limiting government subsidies for the raw material requirements of state economic enterprises.

A focus on fiscal soundness usually complements other SOE reforms. Of the 21 countries identified in IEG’s portfolio where the World Bank engaged in fiscal soundness reforms related to SOEs, only one had fiscal soundness as its sole focus. For example, a 2008 Ukraine development policy loan combined in its supported actions emphasis on strengthening public finances and improving SOE corporate governance. Fiscal ASA can also accompany other SOE reform interventions, often focusing on debt management, accounting, and auditing.

The Equitable Growth, Finance, and Institutions’ SOE task force recently elaborated staff guidance on this type of support. The guidance advises assessing the fiscal impacts of SOE reforms, the fiscal sustainability of any subsidies, and the links to the fiscal framework. The Macroeconomics, Trade, and Investment GP focuses on improving public finances, oversight, and transparency, including lending that supports financial management and macro-fiscal policy.

Where and How the Bank Group Delivers SOE Reform Support

During the evaluation period, for the energy and financial sectors, World Bank lending predominated, constituting more than 90 percent of the value of the Bank Group SOE reform portfolio in those sectors (table 1.1). World Bank lending and ASA for SOE reform constituted about 87 percent of the activity and more than 90 percent of the financing. Within lending projects, DPOs accounted for 516 of the 898 World Bank lending interventions, and investment operations accounted for 382 interventions. IFC delivered $3.8 billion in investment services support in the two sectors through 61 projects and spent $51 million to deliver advisory services through 59 projects. MIGA delivered about $3 billion through four guarantees. Support for the energy sector accounted for 57 percent of interventions and support for the financial sector for 30 percent, with the rest treating both sectors more broadly.

Table 1 - World Bank Group SOE Reform Projects, Commitments by Institution, FY08-18 (est.)

Source: Independent Evaluation Group portfolio review and analysis.

Note: Due to rounding, volume shares add to 101 percent. ASA = advisory services and analytics; est. = estimated; FY = fiscal year; IFC AS = International Finance Corporation advisory services; IFC IS = International Finance Corporation investment services; MIGA = Multilateral Investment Guarantee Agency; SOE = state-owned enterprise.

IEG found relevant SOE ASA reform support activities in 142 countries and all other support in 119 countries. In the sample, the Bank Group financed operations in 34 countries in Sub-Saharan Africa, 21 countries in Europe and Central Asia, 16 in Latin America and the Caribbean, 13 in East Asia and Pacific, 11 in the Middle East and North Africa, and 8 in South Asia. Although Sub-Saharan Africa was the Region with the highest number of financing projects, East Asia and the Pacific had a higher average per country (5.3). Bank Group financing support to reform SOEs has been focused more on lower-middle-income countries (46 percent) and low-income countries (29 percent), followed by upper-middle-income countries (23 percent). MIGA has the majority of guarantees by value in upper-middle-income countries and by a number of projects in lower-middle-income countries.

The Bank Group supports SOE reform at both the upstream and downstream levels. Upstream interventions—mostly by World Bank lending and ASA and IFC advisory—focus on regulatory frameworks for SOE activities; governance and accountability; and ownership, including privatization and PPPs. Downstream interventions (at the enterprise level) focus on SOEs’ business and operations; corporate governance, ownership, and financial management are also substantial areas of engagement. Upstream support was more frequent in upper-middle-income countries, and support for lower-middle-income countries focused more on downstream reforms.

IFC investment and MIGA guarantees, which make up 9 percent of Bank Group commitments, are oriented primarily toward SOEs’ business and operational aspects and SOE ownership (whether through privatization or PPPs). IFC advisory engages both upstream and downstream, most often in business and operations and the upstream and downstream aspects of SOE ownership. MIGA is engaged primarily in the power sector through support of business and operations and ownership reform.

Given the range of activities and dimensions of reform supported, chapter 2 casts an analytic light on the question of how effective the Bank Group has been and the factors associated with success.

Footnotes:- "Over the years, the rationale for state ownership of commercial enterprises has varied among countries and industries and has typically comprised a mix of social, economic, and strategic interests. Examples include industrial policy, regional development, the supply of public goods, and the existence of so-called 'natural' monopolies" (OECD 2015, 2).

- For example, in China, State-Owned Enterprises (SOEs) account for 57% of corporate debt (valued at 72% of gross domestic product), even though they are responsible for less than 20% of output and employment (Lam et al. 2017). For revenue-generating companies (for example, state oil companies), these losses can take the form of foregone revenues to the government.

- "Compared to other companies, SOEs [state-owned enterprises] have specific corruption risks because of their closeness to governments and public officials and the scale of the assets and services they control. Some of the biggest recent corruption scandals have involved state-owned enterprises, which clearly shows the risks that these companies face. In Brazil, the state oil company Petrobras was the focus of a major corruption scandal involving illegal payments to politicians and bribes that affected the whole country. The Nordic telecoms giant Telia was recently caught bribing for business in Uzbekistan, which resulted in fines of $965 million" (Transparency International 2017).

- A recent International Monetary Fund study of emerging Europe found that the "profitability and efficiency of resource allocation of SOEs lag those of private firms in most sectors, with substantial cross-country variation. Poor SOE performance raises three main risks: large and risky contingent liabilities could stretch public finances; sizeable state ownership of banks coupled with poor governance could threaten financial stability; and negative productivity spillovers could affect the economy at large" (Böwer 2017, 2).

- "There seems to be a credible empirical basis for selecting a threshold power system size and per capita, income level below which unbundling of the power supply chain is not expected to be worthwhile" (Vagliasindi 2012b, 22).

- Subsequent to the completion of the analysis for this evaluation, the International Finance Corporation (IFC) provided supplementary portfolio information that the Independent Evaluation Group (IEG) has analyzed. This information suggests that an additional 23 IFC projects could fall into the SOE reform categories, although they were not identified by IEG through consistent application of its methodology. In terms of areas of activity, 37% of the projects were in business and operations, 22% in SOE ownership, and 26% in enterprise-level financial management. Their inclusion was not possible given the late date of receiving this information and would have only marginally changed the picture of IFC's pattern of engagement. One additional evaluated project was identified; it was rated "unsatisfactory."

- In the financial sector, IEG found examples of IFC supporting the restructuring and rehabilitation of state-owned financial institutions' debts through strengthening the asset-liability structure and improving accessibility and pricing of alternative funding sources; the Multilateral Investment Guarantee Agency (MIGA) providing a guarantee for asset-liability management purposes through a US dollar-local currency swap arrangement; and the World Bank supporting a financial restructuring process of SOEs and supporting actions to reduce SOEs' fiscal liabilities. World Bank projects also supported government acquisition, restructuring of debts, and recapitalization of state-owned banks. In the energy sector, the IFC has advised financial restructuring in the power sector in São Tomé and Príncipe, and the World Bank has supported identifying options for restructuring electric companies, actions to bring new shareholders and investments, debt restructuring processes including tariff reviews, clearance of arrears, evaluation of assets, adoption of operational efficiency models, and realignment of roles and responsibilities.

- External incentives shaping corporate behavior include the business enabling environment, the functioning of financial and labor markets, product and input market competition, and the "market for corporate control." See Stone, Hurley, and Khemani 1998.

- "When multiple companies compete head to head for consumers, a market discipline emerges, along with pressure to keep costs down to efficient levels and to improve service quality. The large economies of scale in the power sector mean that key activities (for example, transmission) are traditionally considered natural monopolies, making it inefficient to have more than one supplier. Even under a natural monopoly, however, it is still possible to have different companies compete for the right to supply the market on a monopoly basis for a certain period of time. The liberalization of the power sector therefore often proceeds in incremental stages, beginning with the opening up of generation to independent power producers that compete for the market. Eventually, it may transition to a full single-buyer model where generation is fully divested from the incumbent utility, with the latter acting as the single buyer of generation on behalf of end consumers. The next stage - once the transmission segment has been fully unbundled - is to allow third-party access to the power grid so large customers can purchase power directly from generators on a bilateral negotiated basis. In due course, it may evolve into a wholesale power market, with a centralized price-setting mechanism and a variety of contracts and products being exchanged. In some instances, a final step would unbundle the distribution and retail functions of the utility, allowing the latter to be open to competition for energy supply" (Foster and Rana 2020, 48-9).

- Although competitive neutrality was formalized as a policy in the 2017 IFC Board paper, that paper stated it as an existing principle of IFC investment in SOEs. A 2015 IFC directive, "Investments in State-Owned Enterprises," clearly establishes the requirement to consider "whether or not the IFC investment avoids (i) displacement of viable private provision of the products or services provided by the SOE and (ii) cement of private financing to the SOE." It further requires that an SOE operate in a commercial manner, have operational autonomy from the government, and be subject to commercial and corporate laws applicable to private companies (IFC 2015).

- IFC notes in comments to IEG: "IFC has a robust policy assessment matrix in place to evaluate each SOE investment's fit with IFC's private sector mandate and this assessment is required for all SOE projects. Competitive neutrality plays an important but not an overriding role in this assessment, which includes other variables such as the commercial nature of operations, non-displacement of private alternatives, and operational autonomy from the government."

- MG-010-FY14. MIGA Guidance: Rating State-Owned Enterprise Risk. June 30, 2014; MG-014-FY15. MIGA Guidance: Eligibility Guidance Relating to NHFO-SOE Coverage. August 8, 2014; MG-001-FY2016. MIGA Guidance: MIGLC Frequently Asked Questions. August 3, 2015. Attachment 1. Question 49, pages 25 to 26. In a now superseded 2003 Board statement, the Multilateral Investment Guarantee Agency (MIGA) stated: "It should be stressed that the SOEs MIGA is covering: a) operate on a commercial basis, and b) retain the commercial risks for the projects that MIGA is guaranteeing."

- "In Slovenia, the state owned not only a sizeable portfolio of non-financial companies but also the three largest domestic banks and holds about 63% of the total banking sector's equity. After the first hit of the global financial crisis, Slovenia experienced another banking crisis in 2012-13, when the mostly state-owned banking system came under pressure and led the sovereign to lose market access. Cross-enterprise ownership structures with SOEs at their heart, and pervasively connected lending were believed to have amplified the crises. As a result, bankruptcies were wide-spread, and mounting NPLs [nonperforming loans] ate up bank capital" (Böwer 2017, 15).